Peter Thiel, Scott Cook, and Elon Musk have all spoken out about why b-school grads hurt rather than help innovation. But is it really true?

If you want to be an innovator or an entrepreneur, should you go to business school? At first glance, maybe not: Peter Thiel once said “never ever hire an MBA; they will ruin your company.” Meanwhile, Scott Cook, founder and leader of Intuit, recently told me, “When MBAs come to us we have to fundamentally retrain them — nothing they learned will help them succeed at innovation.” Perhaps a stronger indictment comes from Elon Musk, founder of Tesla, SpaceX, Solar City and PayPal, who said, “As much as possible, avoid hiring MBAs. MBA programs don’t teach people how to create companies … our position is that we hire someone in spite of an MBA, not because of one.”

While we generally recognize that management training has value, why do leaders of innovative companies offer such harsh criticisms?

I would argue that the fault doesn’t lie in the person but in the purpose of management itself. Business schools teach management principles that were developed in the later industrial revolution to solve the large-company management problem — not the innovation problem. As the industrial revolution transformed the economic landscape, replacing small workshops with large companies, the “new giants” created demand for management to make the trains run on time. Business schools followed close behind, with tools to train managers on how to coordinate and control these growing industry titans. However, while these more familiar management practices work well for relatively familiar problems, such as how to optimize activities and coordinate execution, increasing evidence suggests these techniques work poorly for managing the comparative uncertainty of bringing a new idea to market. In other words, business schools have focused on how to capture value from customers, not how to create value.

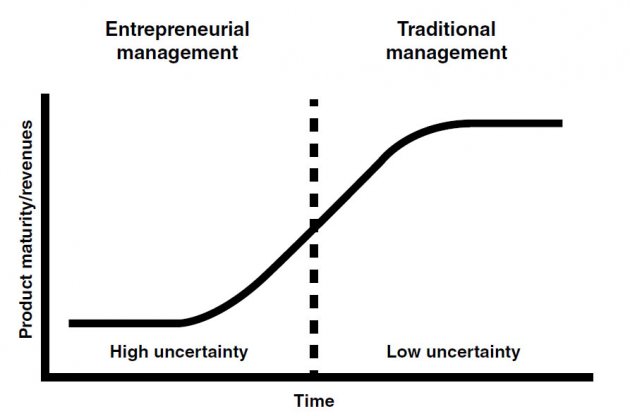

Another way to think about it would be examine the traditional S-curve that describes the life of a product or company (see Figure 1):

(Figure 1)

Early in the life of a company, during the startup phase, uncertainty is high and the entrepreneur is forced to wear a dozen hats to create value. Core tasks include search and discovery in an effort to create a customer. But once that uncertainty begins to resolve, the core tasks shift to execution and optimization in order to capture value. The founders are often kicked out of the company during this shift, and MBAs take the reigns to scale up the company.

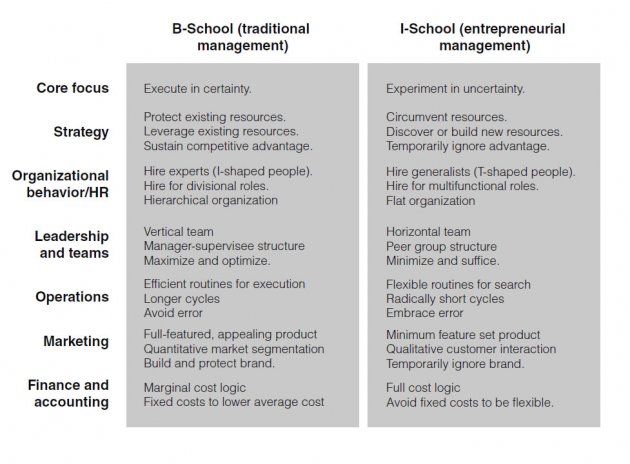

When we talk about conditions of high uncertainty, we need what we might call an innovation school, rather than a business school, approach. An innovation school deals with the emerging science of managing uncertainty. Figure 2 shows the differences between these two schools of thought:

(Figure 2)

To provide an example of how these schools differentiate, consider the following:, In business school (B-school), when you study marketing, you typically learn the importance of building and protecting your brand or doing quantitative analysis to identify customer segments and get customer feedback. In an innovation school (I-school), however, you should initially ignore your brand and obtain all customer feedback through direct interaction, whether by experience, observation or interviews. What’s more, rather than emphasize building brands by satisfying a broad range of customers through perfected products, I-school emphasizes the need to test low-fidelity prototypes with small groups of customers, embracing errors as opportunities to learn.

Further illustrating this point, in B-school, when you learn finance, you’re taught about marginal cost logic: the importance of leveraging prior fixed-cost investments with new initiatives. But this approach biases you toward incremental innovation efforts. In I-school, you learn how to look for opportunities to build something disruptive, something that hasn’t been built before, to deliver a unique solution. In a world of uncertainty, leveraging investments can often be a bad practice because it may lead to building a workaround solution instead of one that nails the job to be done.

I’m not saying that one approach is good and the other is bad. Both are good. The key to success is to recognize when to apply a more familiar B-school approach and when to apply I-school thinking — a decision that rests primarily on the degree of uncertainty. In other words, when uncertainty is high, apply an I-school approach. When the uncertainty has been resolved, use a B-school approach. Fortunately business schools are starting to adopt these ideas, but we are in the midst of a transition. The real question is, how do you manage uncertainty? Are you applying the right process?

Participating in an innovation tournament is a fun and effective way for aspiring entrepreneurs to practice how to leverage resources and take actions to create value.

Based on STVP’s successful Global Innovation Tournament (GIT), this fast-paced, multi-day competition offers teams a chance to solve a mystery challenge to create as much value and impact as possible.

Help students learn skills for idea generation, teamwork, problem solving and value creation, all in an environment of ambiguity and resource constraints.

The educational purpose of the competition is to simulate the experience of being an entrepreneur, in an activity that is suitable for students of all ages. This means learning and developing skills for idea generation, teamwork, problem solving and value creation, all in an environment of ambiguity and resource constraints.

In past years at Stanford, the tournament challenge was to create value from common, everyday objects, such as “sticky notes,” rubber bands and water bottles. The challenges can also be concept-based, such as “Make Saving Money Fun.”

What’s Involved?

As an organizer, you will select the tournament challenge, set the schedule and organize judges and prizes. You will also promote the tournament challenge online or assign the challenge to local students.

Once the challenge has begun, students will have just a few short days to create as much value as possible around the challenge and to upload a video to YouTube to show a record of their progress.

Once the challenge has begun, students will have just a few short days to create as much value as possible around the challenge and to upload a video to YouTube to show a record of their progress. At that point, judges will evaluate the video entries and winners will be selected.

Try placing emphasis on having fun and unleashing student creativity rather than on any competitive aspects of the tournament.

If you are assigning an innovation tournament as part of a university course, the time period just after mid-term examinations seems to be optimal for performance.

Teams can be of any size, from one person to many. Also, we suggest giving students somewhere between four and seven days, including a weekend, to complete the challenge and upload their video.

Prize Suggestions

Wait to pick your award categories until the judges have seen all of the video entries. Name the awards and assign prizes to fit the submissions that warrant recognition.

Reach out to entrepreneurs and business leaders in your local community for experiential prizes. Some ideas include lunch with a startup founder or business executive, or one-on-one meetings with an angel investor or venture capitalist.

Of course, you could also seek out donations of resources to help young entrepreneurs to build the next iteration of their product.

In a recent guest post on the Harvard Business Review website, economic strategist Umair Haque took Silicon Valley venture capital firms to task for backing companies that only create “thin value.” Haque suggests Zynga and Facebook as examples of “light-weight, feel good” companies, who, though popular, do not actually create “thick” value capable of powering economies on a global level. Haque describes this lack of VC interest in “thick” value creation as disruption deficit disorder. His argument may or may not be true, but it actually raises interesting questions for entrepreneurs.

Do VC firms focus on ideas that can scale quickly and turn profits for investors? Sure. If an entrepreneur pitches a compelling business model, an easy-to-build-and-scale prototype, and low projected startup costs, investment firms will likely be interested. However, if an entrepreneur pitches an idea that could create “thick value” through disruptive technologies, but also requires massive funding, within a business model that assumes working in the red for a long period of time, VCs will have reservations. These are venture capital realities. The fact that your idea could contribute to developing new industries and sustained job growth does not really enter the picture. Is this solely the fault of venture capitalists? Maybe the “Disruption Deficit” starts somewhere earlier in the process. Does the founder or entrepreneur play a role in this?

When an entrepreneur discovers an amazing new idea or technology, the “a-ha” moment rarely involves running the idea through a social value filter. Although some “social entrepreneurs” may come from this perspective, the vast majority of entrepreneurs do not lead with this type of thinking. Bare-knuckle technology entrepreneurship goals usually focus on two things: amazing technology applications or an amazing market opportunity. Of course, it’s nice when both come together at the same time. Moreover, it’s hard enough to pull off smart execution in either of these two areas. But are there other factors to consider, perhaps even an approach that can help you achieve financial goals by thinking about social impact first. In the clip below, Guy Kawasaki explains why seeking to build meaning may be the best thing to focus on when starting a company.

Now, maybe you think this whole discussion is of little concern. You’re saying, “there’s already too many things I have to worry about as a bootstrappin’ entrepreneur.” However, what if making a deeper value impact, beyond financial profit, is actually an opportunity. Discovering an idea that can be financially successful and benefit society is really just a bigger challenge. But if startup founders and entrepreneurs won’t take on this challenge from the very beginning of the idea development process, it won’t matter when you get to venture capital funding, since the idea will already be missing thick value creation as part of its design.

During our Entrepreneurial Thought Leader seminars, many of our Stanford engineering students (read: budding Stanford entrepreneurs) ask a variation of the following question to our speakers: If you were going to start a business right now, what would it be? In that question, you can hear the churning wheels of desire for financial success. However, this type of thinking is a version of selling yourself short. Investors discuss the concept of leaving money on the table. As an entrepreneur, have you ever considered that your quick-to-market idea is leaving innovation on the table? Are you selling your creative technical skills short by just creating a “thin value” variation on an existing idea? If you develop a check-in service for retail shops that lets users earn badges and discounts… well, that’s nice. There will be many competitors, and we wish you the best of luck. However, maybe you’re leaving something on the table – that bit of extra brilliance that is needed to help change the world.

The Stanford Technology Ventures Program serves as the entrepreneurship center for Stanford’s School of Engineering. Teaching entrepreneurship to engineers is critical because engineers and scientists are the very people positioned to bring brilliant technical knowledge to the effort of creating thick value. These professionals can raise their technical gifts to an entirely different level by pursuing challenges that will change the world. It’s not about whether you have a moral compass to guide your technological prowess, or whether VCs are interested in funding your idea. It’s about whether or not you are willing to step up to a truly big challenge: Use your technological gifts to build scalable concepts that treat improving society as a given requirement, rather than an optional by-product.

Look at the society around you; are you ready for a real challenge? It’s really up to you.